Mandatory Long-term Care insurance - German:Pflegepflichtversicherung - is an independent part of every German health plan, and goes hand-in-hand with medical insurance.

The intention of the German government in 1995 was to implement insurance compulsory to all of their long-term residents, with the purpose to make sure that if nursing care becomes necessary, financial provisions are in place. Well meant, it must be noted that despite improvements over the years it still provides merely basic coverage, consequently only parts of actual costs are covered.

Brief description of benefits

Implemented in the German Social Security Book XI, the scope of cover is clearly defined for both statutory ("Public") and private insurer and level of care is based on 5 different degrees of care requied. These individual Care Grades include the following benefits:

| Care Grade I | Care Grade II | Care Grade III | Care Grade IV | Care Grade V | |

|---|---|---|---|---|---|

| Home care | --- | 796€ | 1,497€ | 1,859€ | 2,299€ |

| Care allowance | --- | 347€ | 599€ | 800€ | 990€ |

| Daypatient care | --- | 721€ | 1,357€ | 1,685€ | 2,085€ |

| Inpatient care | 131 € | 805€ | 1,319€ | 1,855€ | 2,096€ |

| Short-time care | For those in the Care Grades II to V, related expenses for short-time care in full-inpatient facilities (e.g. clinic) and for a max. of 8 weeks per calendar year, are reimbursed up to a total of 3,539€ per calendar year. | ||||

| Relief amount | Expenses for quality-assured benefits and such to relieve relatives providing care are insured up to 131€ per month. | ||||

| Prevention care | For those in the Care Grades II to V, expenses for a surrogate nurse for up to 6 weeks per calendar year are refunded up to a total of EUR 1,612€ per calendar year. | ||||

| Nursing aids | Reimbursement of costs for necessary nursing aids, provided on rent basis primarily and in accordance with the Nursing Aid Index (German: “Pflegehilfsmittelverzeichnis”). | ||||

| Conversion measures | Allowance of up to 4,180€ to modify housing to suit nursing requirements. | ||||

| Residential groups | Payment of a monthly allowance of 224€ for ambulatory nursing care in supervised outpatient residential groups. Possibility of seeding 2,613€ capital, e.g. to initiate conversion measures in a mutually used residential home to make the residential group even possible. | ||||

worth knowing

Determining the degree of required nursing care

To receive benefits from compulsory long-term care insurance the degree of required long-term care must first of all be determined.

For this purpose, private health insurers rely on the expertise of the joint assessment service called 'Medicproof'. Experts evaluate the level of long-term care, which always depends on how autonomous the person is in managing various areas of life. Among other criteria, mobility, communication - whether requirements can still be expressed at all -, social behaviour and, e.g., whether medication can still be taken are tested independently. The total result makes up one of the five nursing care degrees, which ultimately determines the amount of benefits the insured person is entitled to.

Waiting Periods

The waiting period applies to benefits for both outpatient and inpatient care and since 1. July 2008 the rule is that the insured person must have paid towards statutory long-term care insurance for at least 2 full years within the last 10 years to be able to claim for benefits. Hence, the deferred period one needs to bear in mind is 2 years!

For co-insured children the waiting period is deemed to be fulfilled as soon as one parent has fulfilled it.

People Exempted

Not subject to compulsory private long-term care insurance are those already in need of continous inpatient nursing care in accordance with certain regulations, e.g. due to an accident at work or war victims. Also, privately insured persons who live abroad - outside of Germany - are also generally not required to have long-term care insurance.

Situation for Expats

Short-term residency:

Residing in Germany on a provisional permit (VISA), the Residence Act exempts those from the obligation to insure themselves against long-term care events for the first 60 months of their stay. Although the German Residence Act §2(3) states that the livelihood of a foreigner is secured if adequate health insurance can be paid for without recourse to public funds, hence one would assume this includes Long-Term Care insurance (LTC), looker closer into legislation poves this assumption to be wrong.

The term ‘Health Insurance’ in Germany is defined by inter alila the inclusion of both medical and long-term care insurances, however latter is in fact exempted as its purpose is to secure exceptional safeguarding reasons, see German Residence Act §68 (1,1). Therefore it is in principle generally not part of the means to secure ones livelihood under residence law.

There are circumstances of individual cases in which the Foreigners’ Office can make LTC a requirement, but these are on a discretionary basis and only ever implemented when e.g. the person is already in need of special care.

A circular from the ‘Ministry of Internal Affairs and Municipal Issues’ confirms the above (link).

Long-term residency:

Long-Term Care becomes mandatory to all those who are no longer classed as short-term German residents - after the initial 60 months of residency – consequently should their permit not be extended, they must initiate the application for long-term residency and until approved, are classed as “tolerated” in Germany. To receive approval one part of the requirements is fully substitutive health insurance and this is when people need to find a German health insurance solution.

Important note:

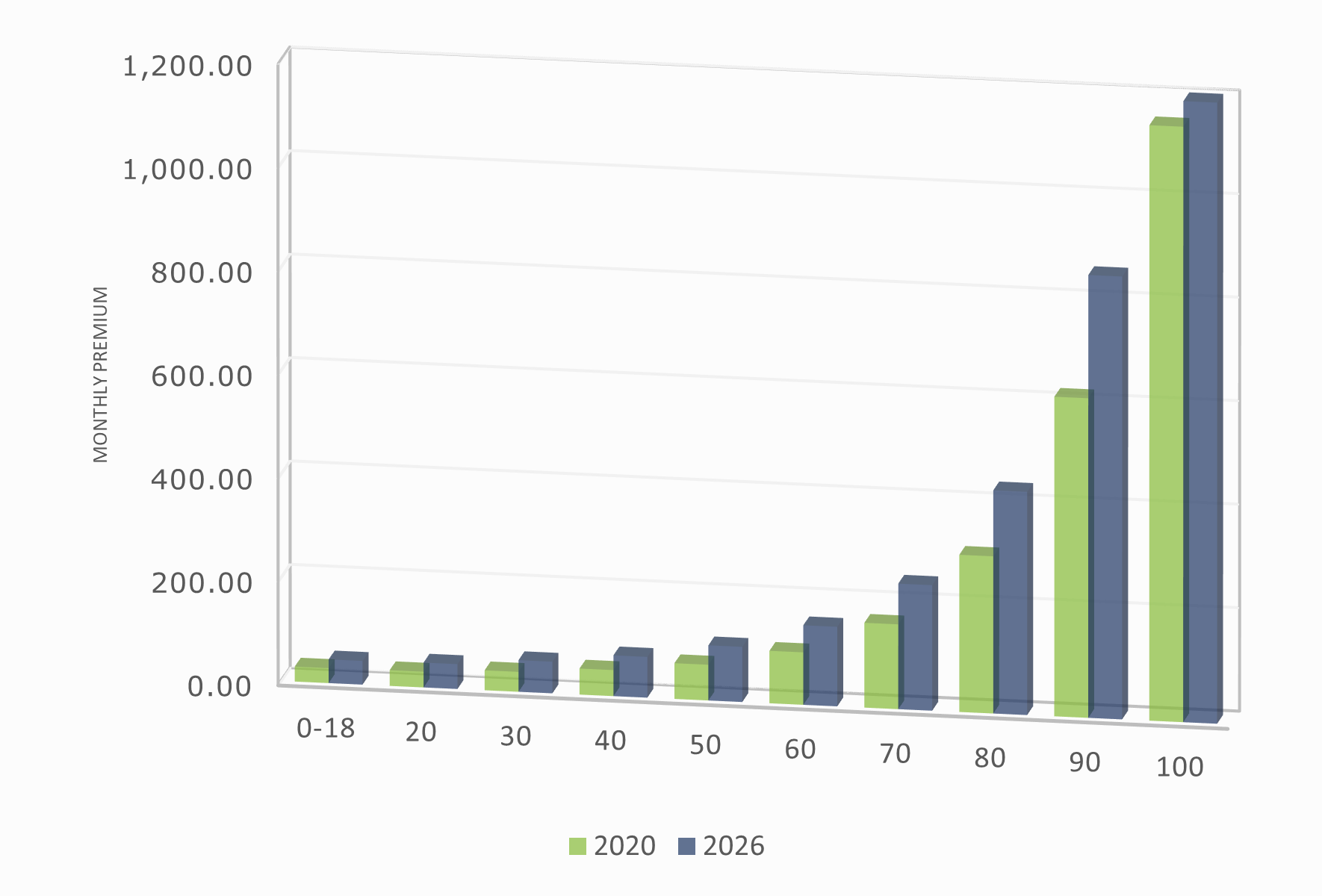

Once the waiting period is no longer an issue, it is possible to leave Germany and claim for benefits as long as you return within 7 years and 11 months.Pricing examples of a German private insurer

| Age | Monthly Premiums | Monthly Premium Development 2020 versus 2026 |

|---|---|---|

| 0 - 18 | 45.82 |

|

| 20 | 48.05 | |

| 30 | 61.61 | |

| 40 | 78.81 | |

| 50 | 106.61 | |

| 60 | 126.96 | |

| 70 | 153.76 | |

| 80 | 242.63 | |

| 90 | 855.73 | |

| 100 | 1,446.11 |

Articles about Statutory Long-term Care

As of 1st July 2023 German legislation stipulates that parents with several children are to contribute less towards mandatory long-term care insurance!

Read Article